“If you can’t fault the assumptions, it’s logical to accept the conclusions”.

In this article, I will address what I regard as the single biggest value add provided to our clients over my years of advising – the power of lifelong cashflow modelling – live. It either provided peace of mind that they were on track, or early warning signs that things needed to be adjusted.

Last month, I wrote about the three roles the new adviser fulfils. The aim is to focus on your clients and on their desired outcomes, not on their money, and you can demonstrate this by articulating three specific roles you play or hats you wear in this order:

Role 1: ‘Life-First’ Discovery – what life do they want to lead, what are their goals, and when?

Role 2: ‘Life-First’ Strategy – are they on track? What strategies and trades off can optimise this?

Role 3: Product Recommendation – only once the strategy is broadly agreed, will it indicates whether the client needs a certain financial product or investment. Financial products are just tools in your kit bag, to be used when or if required. But the real value is in the ‘life-first’ process.

As we discussed last month, we get judged and build trust by the quality of the questions we ask. We touched on some of those key questions, and the biggest question…how much is enough? How much do you need to enable you to live the life you want without fear of running out of money? What’s your ‘number’?

The power of lifelong cashflow modelling

Much of this approach can be achieved through effective use of client-focused financial forecasting or lifelong cashflow modelling software – done live, face to face with our clients; not inserted into a back page of an SoA.

Used properly and with prudent assumptions, this software enables you to show clients in an engaging and thought-provoking way what their future might look like under varying assumptions.

So you could show them that they really can afford to take that world cruise, help their kids with a home deposit, or take redundancy. Retired clients can be shown that they can easily afford to keep the heating on in the winter. Pre-retired couples can be reassured that they can afford to retire now and spend time together while they are still young and fit enough to enjoy it.

By showing clients they are never going to run out of money, you can help them avoid taking unnecessary investment risk and increase their peace of mind. There’s no longer any need to try to shoot the lights out or put yourself under unnecessary stress by promising returns you are never going to be in a position to deliver reliably.

So how do we do it and what does the conversation look like?

“You can have anything, but you can’t have everything”. After all, life is a series of trade-offs.

What we are talking about here would take place typically in a second meeting; a strategy meeting, after all the fact finding has been complete (or once they have become clients, at a Regular Progress Meeting (note we don’t use the term ‘Review’ – we are looking through the windscreen, not the rear view mirror). You will have already completed building financial models and multiple scenarios on your software, prior to the meeting and you are ready to meet with your clients.

Use a screen – the larger the better. A larger TV, projector screen, or smart board. The keys are the numbers and graphs are all clear and legible, and all eyes are all focused on the same point.

Below I will gives some examples of the phrases and terms that have resonated and impacted best. The starting points of course, is that “if you can’t fault the assumptions, it is logical to accept the conclusions”; your client’s role is to continue to fault the assumptions, until they can no longer.

Your role in-essence, boils down to three things:

- helping your client to see clearly where they are now – especially in financial terms

- helping them to identify where they want to be at some future date

- trying to come up with some improved ways of getting them from where they are to where they want to be.

When we talk about where they want to be at some future date, what I mean is: How they want to spend the rest of their life – and what will it cost.

Expenditure

Desired Future Lifestyle: This is the time the client can dream about how they would like to spend the rest of their life, and define it today’s dollars. You should concentrate on three things:

- increase their income & decrease expenses

- reduce their tax liabilities, and there aren’t many legitimate ways, so you shouldn’t waste those which are available, and

- protect their assets and ensure that they and their family are secure in any of the catastrophe situations such as premature death or disability.

Gain some real commitment from them. For example, this means pressing clients when they say “One day, I’d like to…”. Ask them what they mean by ‘one day’. Remind them that time is slipping away and that their life is not a dress rehearsal. This will help you engage with clients in a completely different way – and really connect with them.

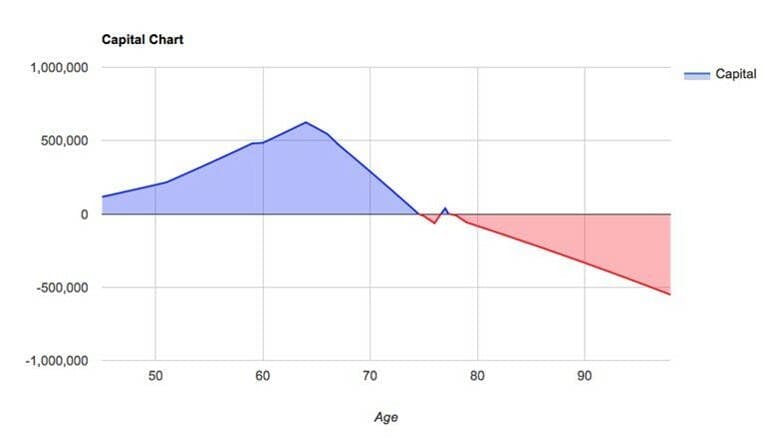

What do we mean by cash flow?

Assets and liabilities are interesting; as is income and expenses. But what we are referring to here is cash flow. My experience is that a cash flow capital chart is the key to client peace of mind.

Your lifelong cash flow modelling will compile the client’s current net worth, including the value of the client’s investment capital. The amount of surplus income will also be calculated. The income and expenditure estimates will generate a lifelong cash flow chart for the client. Normally there will be unacceptable (and probably unexpected) debt levels in retirement. This will create the need for financial planning from the client’s perspective.

Lifelong Cashflow Modelling (click to enlarge). Source: Global Adviser Alpha.

To save getting stuck on points, and to keep the flow of the meeting and address the big picture key points, some words, sayings and best practice tactics to use are listed below, as but examples:-

- If the client states that the information is not known, use the phrase “give your best guess”. This will usually produce some information.

- Don’t let the client distract you from your track, control the meeting by use of such phrases as “we’ll get to that later”. Make a note and come back to it.

- When considering expenditure at the desired future lifestyle:- ask the client if you can assume they will live in the same house, or a house of similar size and position. If the answer is yes, then the house-related expenses will be the same, and time may be save by entering the same values for such expenses as rates, etc.

- Do not gloss over the help-in-house item. Would you like to keep open the possibility of some help in the house? Check the hourly cost of this service in your area, so that actual values may be entered.

- For holidays, without asking enter a value of say three times the current expenditure, look quizzically at the client with a finger poised above the “enter” key. Check the reaction – it’s their life and you are trying to help them.

- For eating out, use the following process, “Just imagine…. you’re 60 tomorrow…, you’ve all the time in the world…, you’ve been a client for years and years, so you’ve no financial worries (smile)…, how many times per week would you like to eat out? 2…? 3…? 4… ? And how much would you spend on a typical night out, including drinks?” Now, multiply the two numbers together and insert that figure into the expenditure.

- If there is a reasonable amount allowed for wines & spirits, the client obviously appreciates such things. Increase the amount by at least 50%, and look at the client for confirmation.

- With increased leisure at retirement, there will be more time for hobbies, sport & entertainment. The allowances for such activities should be increased as well as the magazine subscriptions.

- Long Term Care. Include, as an option, the cost of long term care. Everyone needs to allow for this – anyone can be involved in say a car accident.

Present yourself to the client as a buying service – never as a selling service. Having identified a need, ask if you can buy the product on the client’s behalf. A small point, but one which seems to be appreciated by the clients.

Some other key points and sayings are…

- If we were meeting 3 years from today, what position would you like to be in to be happy with your progress?

- What would need to happen in order that…..?

- Risk/insurance – we could transfer this risk to a life office, but our philosophy is we don’t want you to spend money on insurance if you don’t have to – so let’s re-look at the assumptions

- If you can’t exclude it, you must include it

- In principal….

- Would you like to totally exclude….

Finally, never restrain from stating the obvious; and the ‘Rumpole Principal’ suggests you should never ask a question that you don’t know the answer to. You need to know your numbers, your software, and likely outcomes of changes.

Unlike table 1 above, table 2 shows based on prudent assumptions, our client will pass away with too much money, whereas they could have done more such as travelled business class, helped the kids with home deposits etc, whatever was important to them. The modelling empowers them to see this.

To save getting stuck on points, and to keep the flow of the meeting and address the big picture key points, some words, sayings and best practice tactics to use are listed below, as but examples:-

- If the client states that the information is not known, use the phrase “give your best guess”. This will usually produce some information.

- Don’t let the client distract you from your track, control the meeting by use of such phrases as “we’ll get to that later”. Make a note and come back to it.

- When considering expenditure at the desired future lifestyle:- ask the client if you can assume they will live in the same house, or a house of similar size and position. If the answer is yes, then the house-related expenses will be the same, and time may be save by entering the same values for such expenses as rates, etc.

- Do not gloss over the help-in-house item. Would you like to keep open the possibility of some help in the house? Check the hourly cost of this service in your area, so that actual values may be entered.

- For holidays, without asking enter a value of say three times the current expenditure, look quizzically at the client with a finger poised above the “enter” key. Check the reaction – it’s their life and you are trying to help them.

- For eating out, use the following process, “Just imagine…. you’re 60 tomorrow…, you’ve all the time in the world…, you’ve been a client for years and years, so you’ve no financial worries (smile)…, how many times per week would you like to eat out? 2…? 3…? 4… ? And how much would you spend on a typical night out, including drinks?” Now, multiply the two numbers together and insert that figure into the expenditure.

- If there is a reasonable amount allowed for wines & spirits, the client obviously appreciates such things. Increase the amount by at least 50%, and look at the client for confirmation.

- With increased leisure at retirement, there will be more time for hobbies, sport & entertainment. The allowances for such activities should be increased as well as the magazine subscriptions.

- Long Term Care. Include, as an option, the cost of long term care. Everyone needs to allow for this – anyone can be involved in say a car accident.

Present yourself to the client as a buying service – never as a selling service. Having identified a need, ask if you can buy the product on the client’s behalf. A small point, but one which seems to be appreciated by the clients.

Some other key points and sayings are…

- If we were meeting 3 years from today, what position would you like to be in to be happy with your progress?

- What would need to happen in order that…..?

- Risk/insurance – we could transfer this risk to a life office, but our philosophy is we don’t want you to spend money on insurance if you don’t have to – so let’s re-look at the assumptions

- If you can’t exclude it, you must include it

- In principal….

- Would you like to totally exclude….

Finally, never restrain from stating the obvious; and the ‘Rumpole Principal’ suggests you should never ask a question that you don’t know the answer to. You need to know your numbers, your software, and likely outcomes of changes.

Unlike table 1 above, table 2 shows based on prudent assumptions, our client will pass away with too much money, whereas they could have done more such as travelled business class, helped the kids with home deposits etc, whatever was important to them. The modelling empowers them to see this.

Critics

Critics would say things such as “how can you project out say 30 or 40 years”, “it can’t possibly be correct, as things will change” and other objections such as this. My view very clearly is that the alterative to making assumptions is to make none at all. And of course things will change – relationships, health, laws, markets, interest rates, the economy, goals and objectives, etc – that’s why before making any big decision, we should update the model and re-run the numbers, at worst each 12 to 18 months, or for any material change in circumstances.

The alternative to doing this is not doing this, and that won’t provide much information at all.

Review Meetings become Regular Progress Meetings

Rather than focussing on reviewing past portfolio performance, instead, your progress meetings can become forward-looking, focusing on what is changing in clients’ lives, how their needs and goals are evolving and how external events play into the plan you have created for them.

The old way in which advisers spent hours boring clients with chatter about investment products and quarterly performance may have worked when clients didn’t know how much they were paying for your service, but not anymore.

Again, you are differentiating yourself by taking the focus off products and investments and putting it on the clients’ lives. From product to people; and from money to meaning.

Empower your clients to make sound decisions. Once you’ve helped clients understand their number, your role is to help them accumulate it, manage it, protect it, and most importantly, enjoy it.

Now think about your value proposition and its impact:

- You have changed your clients’ lives for the better and changed your own life, immeasurably

- You now feel genuinely good about the work you do and experience a real sense of purpose

- You have differentiated yourself from other advisers who focus only on product.

- You have fewer clients, but they are happy to pay you more

- Spending less time on things that don’t matter leaves you with more time to spend on the things that do.

If you acquire mastery in lifestyle financial planning, the ‘money stuff’ becomes less important.

Clients won’t understand proper financial planning until they experience it. But herein lies your opportunity.